A Random Variable Is Said To Be Continuous If It

Juapaving

Mar 18, 2025 · 6 min read

Table of Contents

A Random Variable is Said to Be Continuous If…

A random variable is a variable whose value is a numerical outcome of a random phenomenon. Understanding the difference between discrete and continuous random variables is crucial in probability and statistics. This article delves deep into the characteristics of continuous random variables, exploring their probability density functions, cumulative distribution functions, and key examples. We will also touch upon the practical applications of these concepts.

Defining a Continuous Random Variable

A random variable is said to be continuous if it can take on any value within a given range or interval. Unlike discrete random variables, which can only take on specific, separate values (like the number of heads in three coin tosses), continuous random variables can assume an infinite number of values within a continuous range. Think of measuring height: a person's height could be 175.2 cm, 175.23 cm, or even 175.2345 cm – the precision is limited only by the measuring instrument.

Key Characteristics of Continuous Random Variables:

- Infinite Possible Values: Within its defined range, a continuous random variable can take on any value, even those with infinitely many decimal places.

- Probability at a Single Point is Zero: The probability of a continuous random variable taking on any single specific value is zero, P(X = x) = 0. This might seem counterintuitive, but it's a fundamental property. The probability is distributed across the range, not concentrated at individual points.

- Probability is Measured Over Intervals: Instead of individual points, probabilities are associated with intervals. We calculate the probability that the random variable falls within a specific range (e.g., the probability that a person's height is between 170 cm and 180 cm).

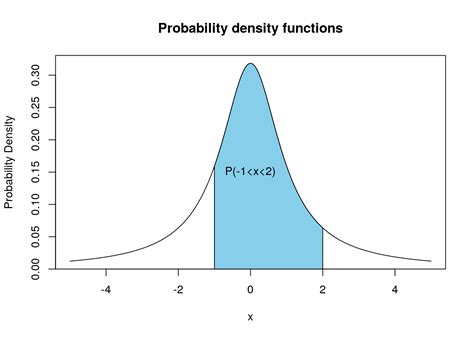

- Probability Density Function (PDF): The probability distribution of a continuous random variable is described by a probability density function (PDF), denoted as f(x). The PDF is not a probability itself; rather, the area under the curve of the PDF over a given interval represents the probability that the random variable falls within that interval.

- Cumulative Distribution Function (CDF): The cumulative distribution function (CDF), denoted as F(x), gives the probability that the random variable is less than or equal to a specific value x. It's the integral of the PDF from negative infinity to x.

The Probability Density Function (PDF)

The PDF, f(x), is a non-negative function that satisfies the following conditions:

- Non-negativity: f(x) ≥ 0 for all x.

- Total probability equals one: The integral of f(x) over its entire range is equal to 1: ∫<sub>-∞</sub><sup>∞</sup> f(x) dx = 1.

The probability that the continuous random variable X falls within the interval [a, b] is given by the definite integral of the PDF over that interval:

P(a ≤ X ≤ b) = ∫<sub>a</sub><sup>b</sup> f(x) dx

This integral represents the area under the curve of the PDF between points a and b.

Examples of Probability Density Functions

Several well-known probability distributions describe continuous random variables. Let's examine a few:

-

Uniform Distribution: In a uniform distribution, the probability density is constant over a specified interval [a, b]. The PDF is:

f(x) = 1/(b-a) for a ≤ x ≤ b f(x) = 0 otherwise

-

Exponential Distribution: Often used to model the time between events in a Poisson process (like the time until the next customer arrives at a store). The PDF is:

f(x) = λe<sup>-λx</sup> for x ≥ 0 f(x) = 0 otherwise

where λ (lambda) is the rate parameter.

-

Normal Distribution (Gaussian Distribution): The most ubiquitous distribution in statistics. Its bell-shaped curve is characterized by its mean (μ) and standard deviation (σ). The PDF is:

f(x) = (1/(σ√(2π))) * e<sup>-((x-μ)²/(2σ²))</sup>

-

Beta Distribution: Used to model probabilities, proportions, or percentages. It's defined on the interval [0,1] and has two shape parameters, α and β.

The Cumulative Distribution Function (CDF)

The CDF, F(x), provides the probability that the random variable X is less than or equal to a particular value x:

F(x) = P(X ≤ x) = ∫<sub>-∞</sub><sup>x</sup> f(t) dt

The CDF has the following properties:

- Monotonically increasing: F(x) is a non-decreasing function.

- Limits: lim<sub>x→-∞</sub> F(x) = 0 and lim<sub>x→∞</sub> F(x) = 1.

- Probability calculation: P(a < X ≤ b) = F(b) - F(a).

Practical Applications of Continuous Random Variables

Continuous random variables are essential tools in various fields:

- Engineering: Modeling the strength of materials, the lifetime of components, or the noise in a signal.

- Finance: Modeling asset prices, interest rates, or the returns on investments.

- Physics: Describing the position or velocity of particles.

- Medicine: Modeling the duration of illnesses or the response to treatments.

- Meteorology: Modeling rainfall amounts, temperatures, or wind speeds.

- Environmental Science: Modeling pollutant concentrations, water levels, or species populations.

Distinguishing Between Discrete and Continuous Random Variables

The core difference lies in the nature of the values the variable can take:

| Feature | Discrete Random Variable | Continuous Random Variable |

|---|---|---|

| Values | Takes on distinct, separate values. | Can take on any value within a given range. |

| Probability | Probability assigned to each individual value. | Probability assigned to intervals; P(X=x) = 0. |

| Distribution | Probability mass function (PMF). | Probability density function (PDF). |

| Examples | Number of heads in coin tosses, number of cars in a lot | Height, weight, temperature, time |

Advanced Concepts and Extensions

The study of continuous random variables extends to more advanced topics like:

- Joint distributions: Describing the probability distribution of two or more continuous random variables.

- Conditional distributions: Examining the probability distribution of one continuous random variable given the value of another.

- Transformations of random variables: Determining the distribution of a function of a continuous random variable.

- Statistical inference: Using continuous random variables to make inferences about population parameters.

Conclusion

Understanding continuous random variables is crucial for anyone working with probability and statistics. Their applications span numerous fields, and mastering the concepts of PDFs, CDFs, and the inherent properties of continuous variables is essential for interpreting and analyzing data effectively. By grasping these fundamental concepts, one can build a robust foundation for tackling more complex statistical problems and developing meaningful insights from data. The ability to model real-world phenomena using these distributions empowers informed decision-making across various disciplines. This article has provided a comprehensive overview, but further exploration into specific distributions and their applications is highly recommended for a deeper understanding.

Latest Posts

Latest Posts

-

What Are All The Factors Of 75

Mar 18, 2025

-

Is A Colloid Homogeneous Or Heterogeneous

Mar 18, 2025

-

What Cell Stores Food And Water

Mar 18, 2025

-

Function Of The Base On A Microscope

Mar 18, 2025

-

Square Root Of 50 Rational Or Irrational

Mar 18, 2025

Related Post

Thank you for visiting our website which covers about A Random Variable Is Said To Be Continuous If It . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.